Based on amounts paid over the past 12 months, the FTSE 100’s currently (28 November) yielding 3.15%. But it has been higher. For example, in 2020, it was over 4%. And the current return is at its lowest level since 2007.

Some of this reduction can be explained by a recent trend towards more share buybacks. According to AJ Bell, companies on the index have announced plans to use £50.9bn of surplus funds to repurchase their own shares. When combined with dividends, analysts are expecting a cash return to shareholders of 5.5% in 2025.

Over four decades of increases

But there’s one stock on the index — Scottish Mortgage Investment Trust (LSE:SMT) — that, according to the Association of Investment Companies, has raised its payout for a remarkable 43 years in a row. In cash terms, its dividend for the year ended 31 March (FY25) was 28% higher than for FY20.

Having said that, it’s also been following the crowd. From March 2024 to 30 September, the trust’s bought £2.6bn of its own stock. However, despite this impressive run of dividend hikes, the stock’s only yielding 0.4%. If I was a shareholder, I wouldn’t be getting too excited about this.

A different objective

But income isn’t what the trust’s all about. Its stated mission is to invest in the world’s “most exceptional” growth companies. At 30 September, its five biggest holdings were Space Exploration Technologies (7.6% of assets), Mercadolibre (5.4%), TSMC (5.3%), Amazon (4.6%) and Bytedance (3.8%).

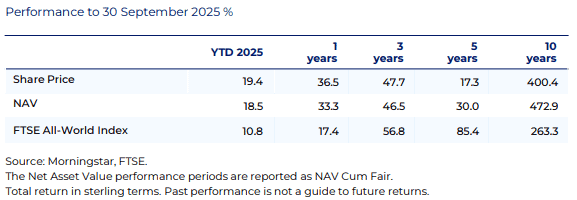

However, since October 2021, the trust’s share price has lagged the performance of the FTSE All-World index. Prior to this, it consistently did better. In November 2021, its shares were changing hands for over £15.

Pros and cons

At the moment, the trust’s shares trade at a 13% discount to its net asset value. This is a strong indication that the stock’s undervalued. However, it also highlights a potential issue that might be concerning investors.

Namely, a significant proportion of its investments, including its position in SpaceX, are in unlisted companies (26.6% of assets at 30 September). These can be difficult to value as there’s no active market for their shares.

Another possible risk is that the trust’s earnings can be erratic. As its manager says, its investing style “comes with a tolerance for volatility as progress is rarely in a straight line”.

But a look at the trust’s holdings is like a who’s who in the world of tech and other high-growth sectors. Many are companies at the forefront of their industries demonstrating strong earnings growth and healthy cash flows.

My verdict

Scottish Mortgage Investment Trust has one of the longest unbroken sequences of dividend increases of any FTSE 100 stock. But I don’t believe it’s worth looking at as an income share. However, for its long-term growth potential, I think it could be one to consider.

Taking a position in an investment trust is a great way of spreading risk. In this case, it’s possible to have exposure to 99 different companies through a single shareholding. It’s a way of owning quality stocks without the hassle of having multiple positions.