Lloyds‘ shares (LSE:LLOY) have quietly delivered a far stronger return than many expected. As a result, a £10,000 investment five years ago now standing at roughly £24,600.

That outperformance reflects a combination of resilient earnings, tighter cost discipline and, crucially, an overly pessimistic set of base-case assumptions that surrounded the bank earlier in the cycle.

Markets spent years pricing in heavy credit impairments as the UK entered successive periods of economic uncertainty. Yet actual defaults remained far lower than the models suggested. This was supported by stable employment, a resilient UK consumer, and households deleveraging more than anticipated.

At the same time, the FTSE 100 company has benefitted from a prolonged period of elevated interest rates. Forecasts once implied that net interest margins would collapse quickly after the initial spike in rates. However, the decline proved far more gradual.

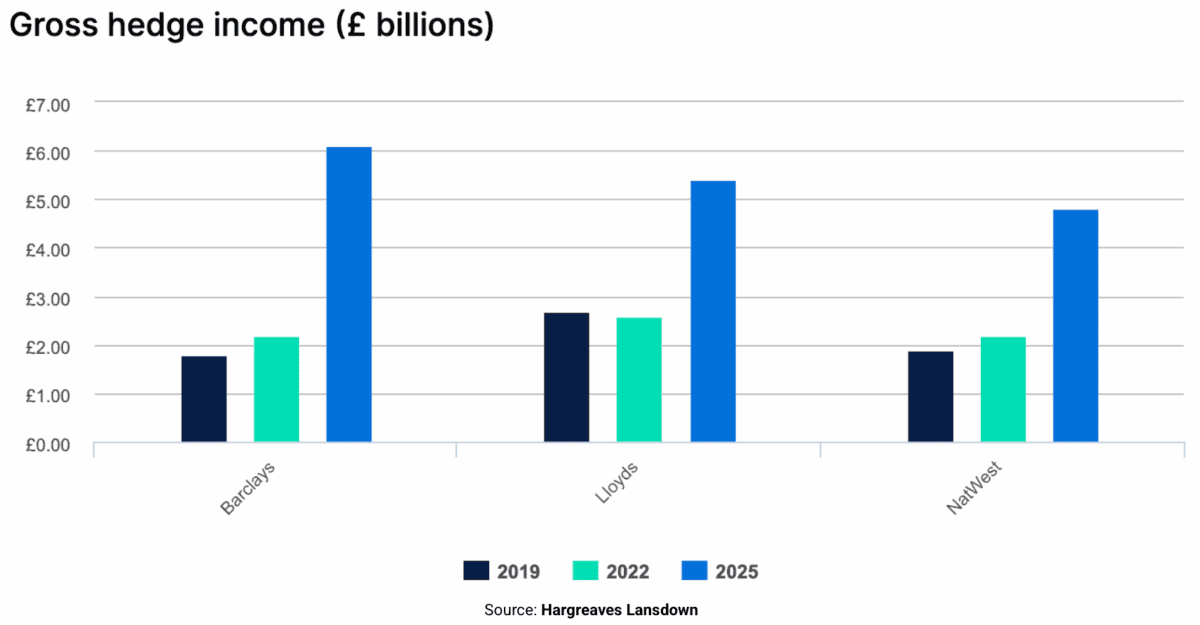

One factor behind that has been hedging. Banks have been replacing lower-yielding hedges (buying things like govt debt) with new contracts struck at materially higher rates. That supported net interest income even as headline rates eased from their peak.

Below is a two-year-old forecast from Hargreaves Lansdown. I’ve used it several times in the past and it’s proven to be very relevant. In Q3 2025, the hedging strategy contributed £1.4bn.

Management has also used that breathing space to clean up the balance sheet, maintain robust capital buffers, and keep shareholder distributions flowing. For example, the bank’s CET1 ratio — a core measure of a bank’s financial strength and stability — is 13.8%. That’s substantially above the minimum requirement.

Combined with steady progress in reducing operating costs and expanding fee-generating activity, the bank has consistently beaten the modest expectations set for it.

The result is strong earnings and a re-rating — in other words investors are happy to the bank trading with a more expensive valuation.

Where now?

Predicting exactly what’s going to happen next is challenging, especially in the week containing the Chancellor’s Budget.

First thing to consider is that banks reflect the health of the UK economy. Sadly, I’m becoming increasingly pessimistic. Financial analyst John Choong’s truly excellent Interpretiv research and newsletter points to a £38bn government blackhole that’s going to require more taxes and spending cuts.

And if inflation does come down as the UK economy cools further, then more interest rate cuts should be on the cards. That might be good for mortgage holders like me, but it will have an impact on net interest income.

These are definitely risk factors for Lloyds, especially if the impacts are more severe than the current base-case scenario. It’s also trading at 12 times forward earnings — the most expensive it’s been in years.

However, it’s proven to be a resilient institution in recent years, capable of generating outsized returns from the UK lending sector. I still think it’s worth considering for the long run, but other options may be cheaper.