Tesco (LSE: TSCO) shares had one of their best runs of the year last week, surging 4.7% in five days.

The boost comes after the grocer upgraded its fiscal 2026 guidance in early October. It reported a 5% year-on-year sales increase, driven largely by Clubcard loyalty schemes and price matching. Considering the lingering pressures caused by stubborn inflation, the growth is encouraging.

And the company hasn’t wasted the opportunity to reward shareholders — dividends are up almost 13% this year, and it’s repurchased a further £1.45bn worth of shares.

But with the shares now trading near their all-time high, is there a risk of a correction? Quite possibly — but I’m still buying more shares anyway. And here’s why.

Safety in a shaky economy

In case you haven’t heard, confidence in the US economy isn’t exactly at an all-time high. In fact, several big names in the finance world have recently voiced their concerns about an impending crash.

As the saying goes: when America sneezes, the rest of the world catches a cold.

Of course, nobody knows for sure what’s going to happen, or when. And the UK, with less exposure to speculative tech stocks, will probably weather a market downturn better than the US. But still, it pays to prepare – and defensive stocks are a great way to do that.

Tesco’s just one of many defensive stocks that I’m rebalancing funds into as 2025 draws to a close. Others include AstraZeneca, Unilever, GSK and National Grid.

These companies all share a similar trait — products and services that remain in high demand even when money’s tight. That makes them less susceptible to market shocks when things get volatile.

Income and value

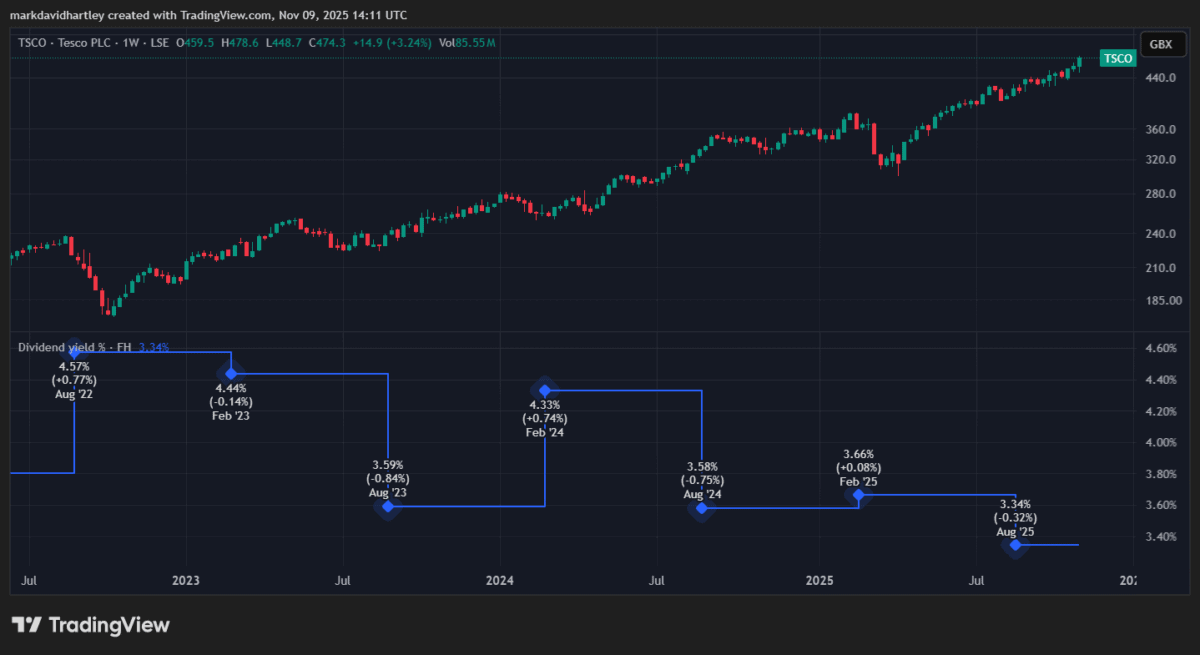

Tesco’s soaring share price has caused its dividend yield to dip slightly this year. Now down to only 3%, it’s the lowest it’s been in over five years.

That could detract some income investors as it’s now lower than the FTSE 100 average.

But the falling yield belies a policy that’s driven average dividend growth of 8% a year since the pandemic. That growth’s expected to continue, even if the share price corrects mildly in the short term.

With strong cash and earnings coverage, I see no reason to fear a dividend cut or reduction in the near future. My only slight concern would be the company’s debt which, at £14.97bn, is notably higher than its equity.

I wouldn’t go so far as to say it’s a risk but I’d feel more comfortable if it were lower.

Final thoughts

At a time when global markets are looking increasingly fragile, Tesco’s performing surprisingly well. It still faces stiff competition from the likes of Aldi and Lidl — lower-cost alternatives which are likely to do better if money gets really tight.

But overall, recent results are impressive, and the combination of share buybacks and dividend growth gives me extra confidence.

I’ve been buying the shares throughout this year and plan to continue doing so as part of a strategy to build a more defensive portfolio. As fears of a stock market crash grow, risk-averse investors may also want to consider defensive stocks like Tesco.