I have a bit of spare cash in my Stocks and Shares ISA at the moment. But inflation’s constantly eroding its value so I’d rather it be deployed in the stock market.

To identify potential candidates, one option I like to pursue is to look at well-known names that have seen their share prices fall significantly over a relatively short period of time.

Of course, this could be a sign of a fundamental problem. But sometimes, it’s an indication of a short-term issue that’s likely to be overcome, although often not immediately.

If all goes to plan, in a few years’ time, it might be possible to look back and pat myself on the back for picking up a bit of a bargain. However, I think it’s important to be patient. A recovery can take time and is rarely smooth.

A fallen giant

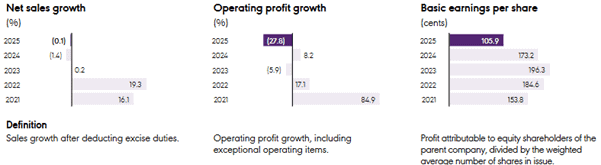

The Diageo (LSE:DGE) share price has fallen 31% since the start of 2025. The stock’s now (31 October) changing hands for around 56% less than when it reached its post-pandemic high in December 2021.

However, the group remains a titan of the drinks industry. It owns over 200 brands – the most famous probably being Guinness — covering all tastes and price points in the market. It was one of the few companies that did well during the pandemic.

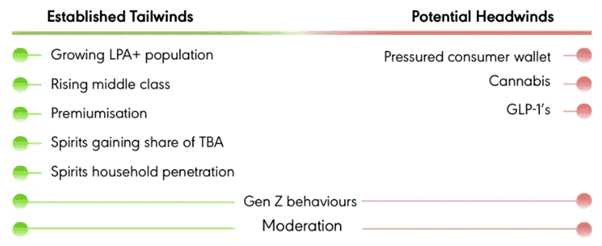

But over the past four years, the group’s seen a decline in its sales volumes. It says this reflects a trend towards drinking better not more. In other words, people are trading up and buying more expensive brands. For example, from 2014-2024, the share of the spirits market accounted for by premium labels increased from 26% to 35%.

Yet I would have expected this to be reflected in an improvement in the group’s gross profit margin. Instead, this appears to be relatively flat and has been in a narrow range of 43.4%-43.7% during its past four financial years.

| Financial year | Reported volume (million equivalent units) | Gross profit margin (%) |

|---|---|---|

| 2022 | 263.0 | 43.7 |

| 2023 | 243.4 | 43.4 |

| 2024 | 230.5 | 43.7 |

| 2025 | 230.1 | 43.5 |

Not all bad

Despite the group’s woes, Guinness continues to be a success story. Thanks to some high-profile ‘Guinnfluencers’ creating plenty of social media interest, it’s been estimated that the brand’s now worth nearly 20% of the group’s total market-cap. And as evidence of changing tastes, the alcohol-free version is doing particularly well. Ocado now sells more 0.0 than it does of the original.

One benefit from the falling share price is that those who invest now could achieve a 4.5% yield compared to the average for the FTSE 100 of 3.3%. This is based on amounts paid over the past 12 months. Of course, there can never be any guarantees when it comes to dividends.

My verdict

On balance, the stock’s not for me. Although Diageo has some impressive brand names in its stable, due to changing tastes and attitudes, I think there’s some uncertainty over the long-term prospects for the drinks industry.

For health and financial reasons, GenZ-ers are drinking less than their parents. And increasingly cash-strapped governments around the world are likely to consider the sector an easy target for additional duties and taxes.

Although I think the group has lots going for it, until I see evidence of a turnaround, I’m not going to invest.