The FTSE 100 rose above 9,500 for the first time earlier this month. Yet despite reaching this milestone, many dividend stocks continue to sport bumper dividend yields.

One such Footsie stock is Aviva (LSE:AV.). Based on current fiscal 2026 forecasts, the insurer is tipped to pay out 41.5p per share. At today’s share price of 659p, that equates to a forward yield of 6.32%.

Considering the Aviva share price is up 40% year to date, that’s still a hearty offering. And 41.5p would represent year-on-year dividend growth of 7.2%, thereby outpacing UK inflation by a decent margin.

Of course, these forecasts might not turn out to be accurate (sometimes they end up wide of the mark). But Aviva’s enjoying strong business momentum right now, with operating profit jumping 22% to £1.07bn in the first half of the year.

Also, the integration of Direct Line is well underway. This combined business will have over 21m customers, or four in 10 adults in the UK. Aviva’s confident this deal will “contribute significantly” to future growth.

Over the past five years we’ve transformed the performance and prospects of Aviva…We are very well positioned to accelerate growth in the capital-light areas of wealth, health and general insurance, and deliver more and more for our shareholders.

Aviva CEO Amanda Blanc.

Admiral

Another FTSE 100 insurance stock forecast to offer decent income in 2026 is Admiral (LSE:ADM). The company’s expected to dish out £2.13p per share, equating to a forward-looking yield of 6.55%.

This would only be 1.1% growth, but Admiral has a solid track record of increasing its annual payout (nearly 8% over the past few years). And dividends have risen significantly since 2023.

The UK motor insurance giant is well-run outfit with excellent underwriting margins and a keen focus on improving its data capabilities to maintain its competitive positioning. In the first half, UK customers rose 13% to 9.3m.

As a major UK motor insurer, Admiral’s exposed to claims inflation (repair costs, labour, parts, etc). Aviva faces similar risks with its beefed-up car insurance business, while both would face challenges from an economic downturn.

Nevertheless, I think they’re top insurance stocks to consider for their long-term income potential.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

REIT

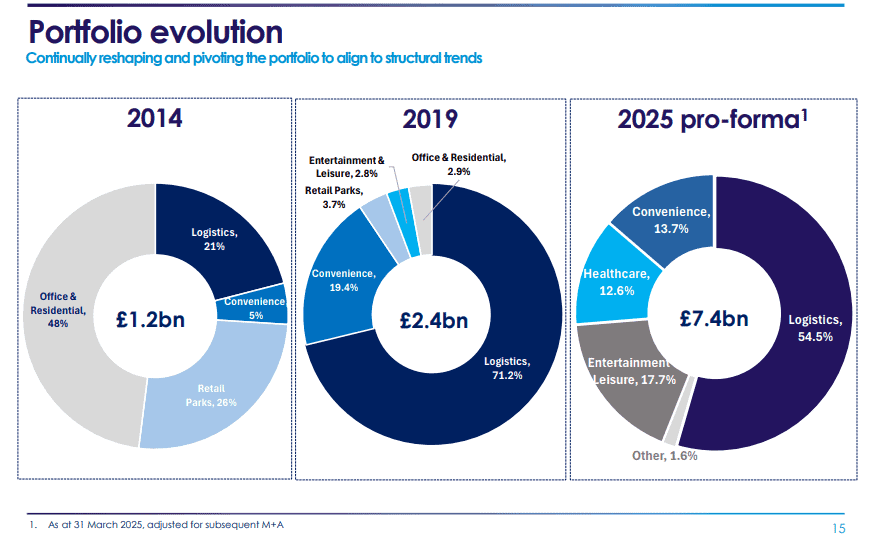

Finally, there’s Londonmetric Property (LSE:LMP). This is a real estate investment trust (REIT) that owns a lot of logistics and warehousing property — the sort of assets that underpin the online shopping economy.

This year, Londonmetric’s dividend is forecast to jump more than 20%. Then it’s tipped to rise another 3.6% next year to 12.9p. At today’s share price of 189p, that would result in a yield of 6.82%.

Of course, property values remain sensitive to higher interest rates, and a UK recession could lead to more tenant defaults. However, Londonmetric’s occupancy rate is high at 98%, and I like that it has been taking advantage of market uncertainty to acquire assets and increase its exposure to logistics.

As shown above, the company has more than doubled its exposure to logistics as e-commerce has boomed over the past decade. It’s also reduced exposure to offices and retail parks, while leaning into areas with more resilience and/or structural growth.

With interest rates expected to fall in 2026, I think Londonmetric, at 189p, is also worth considering for income.