The Associated British Foods (LSE:ABF) share price has turned negative for 2025 following a shocking market reaction to first-half sales.

On Thursday (10 September), the food and clothing giant slumped by double-digit percentages due to underwhelming Primark sales numbers. At £19.51 per share, the FTSE 100 company is now down almost 6% in the calendar year.

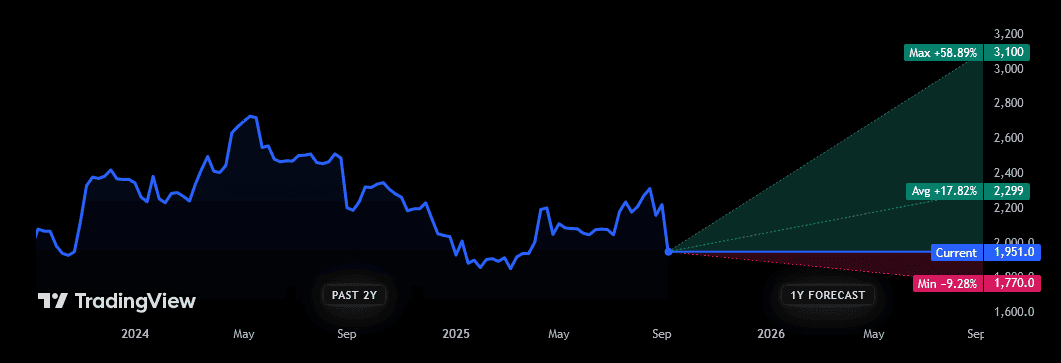

I’m wondering if this represents an attractive dip-buying opportunity for eagle-eyed investors. Encouragingly, City analysts are (broadly speaking) expecting the shares to bounce back strongly over the next 12 months:

But how robust are these forecasts? And, as a long-term investor, should I consider adding the Primark owner to my portfolio anyway?

Key European market splutters

In theory, the company’s focus on value clothing should provide protection against broader weakness in consumer spending. However, the scale of the retail downturn means that even low-cost specialists like this are struggling.

Things aren’t all bad, with Primark reporting a “good sequential improvement” in UK and Irish sales in the second half of the year versus the first. It has also reported “strong” sales in the US in the six months to September.

But trouble persists in Mainland Europe, with sales growth cooling across the territory. Roughly 18% of Primark’s sales come from Spain and Portugal, where sales growth is tipped to slow to 2% for the second half, from 8% in the first.

And in France and Italy, sales are tipped to reverse 4% between April and September. They rose by 4% in the previous six months.

Primark generates 16% of group sales from France and Italy, and 12% from Northern Europe. Here the business is also experiencing trouble, and a 2% top-line decline is being predicted for the second half. Sales rose 1% in the first.

Under the cosh

Recent weakness means Primark’s total sales are now tipped to rise 1% over the second half. That’s below growth of 3%-4% that City analysts had been tipping.

It’s not just problems in Europe, and what this could mean for the company’s expansion strategy that have spooked investors. Trading in the UK and Ireland is robust, but investors fear a slowdown as the UK economy splutters. The same goes for Primark’s small growth region of the US.

From a long-term perspective, I remain optimistic about the company’s retail unit, which provides almost half of group sales. Steady expansion gives it opportunities to capture structural growth in the value retail market. It’s also investing heavily in areas like Click & Collect to capitalise on the e-commerce boom.

However, the scale of Primark’s problems come as some surprise, as Associated British Foods’ share price slump this week indicates. And it’s not just here where the FTSE 100 company is struggling — profitability at its Grocery unit is under strain due to heavy restructuring costs. Meanwhile, the Sugar division remains plagued by weak prices for the sweet commodity.

Given its mounting issues, I’m not convinced the firm’s shares will rebound as sharply as City analysts think over the next year. While I like the look of it over the long term, I think risk-averse investors should consider buying other UK shares instead.