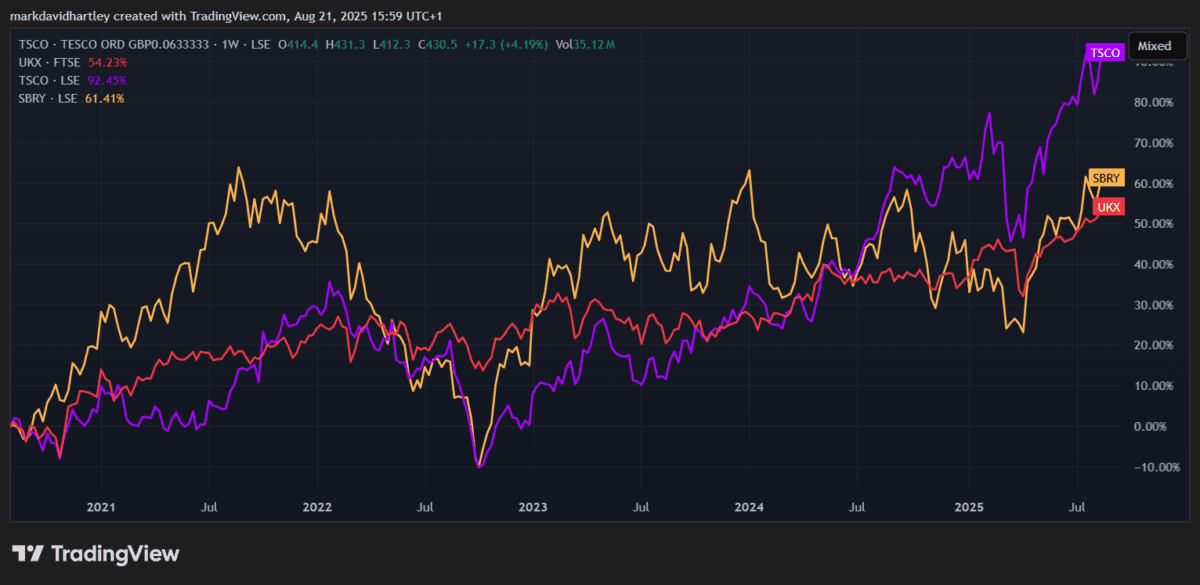

Tesco (LSE: TSCO) shares are up over 90% in the past five years, with the vast majority of those gains coming in just the past two.

After post-Covid inflation began tapering off in 2023, the UK’s largest supermarket chain has gone from strength to strength.

An investor who sank £5,000 into the stock in August 2020 would be sitting on a £2,500 gain from capital appreciation alone. Reinvesting dividends along the way, that figure climbs to around £11,200 in total value – a tasty £6,200 profit.

By comparison, the FTSE 100 has only managed a 54% rise in the same period.

Main rival Sainsbury’s has also delivered a more modest return over the same five-year stretch, with the shares up around 61%. Admittedly, it does have a slightly more meatier dividend though. But even with the benefit of its Argos business and a stronger push into convenience stores, it seems it simply doesn’t have the same scale or buying power as Tesco.

Clearly, things have been going well lately. But will the growth continue or is it now overvalued?

An optimistic market

Last month, Tesco confirmed it will continue with its existing £1.45bn share buyback programme, a signal that management believes the stock is still attractive at current levels. Not long after, Deutsche Bank reiterated its Buy rating, setting a target price of 470p.

Interestingly, that’s exactly where a discounted cash flow analysis would place the stock, suggesting it remains around 10% undervalued today. Citi is also bullish, setting a slightly lower target of 460p. Either way, the analysts are in agreement: the market is still pricing Tesco below fair value.

Cost-of-living crisis

Of course, it’s not all smooth sailing. Britain’s cost-of-living crisis continues to put retailers under pressure. Earlier this month, Tesco joined forces with rivals including Sainsbury’s, Asda, Aldi, Lidl, John Lewis, JD Sports and Boots in writing to finance minister Rachel Reeves. The letter warned that further tax hikes in the Autumn Budget could undermine the government’s pledge to improve living standards.

Meanwhile, it’s quietly nudging prices higher, with its popular meal deal set to rise by another 25p. That might not sound like much, but such moves can irritate customers in an ultra-competitive market.

Some rivals are going in the opposite direction. Lidl, for example, has lifted hourly pay for its 28,000 workers for the fifth time in two years. And from September, Aldi will pay store assistants at least £13 an hour — a fair bit above the £12.21 minimum wage.

Wage pressure like this has the potential to squeeze Tesco’s margins over time.

My verdict

At the end of the day, whether Tesco shares dip in the short term is largely irrelevant to me. I see this as a long-term play that offers a mix of reliable income, defensive qualities and consistent growth.

Yes, it faces challenges in a tight consumer environment, but Tesco’s scale and efficiency give it a moat that few rivals can match.

For me, it’s still a stock worth considering for any well-diversified UK investment portfolio.