Listening to passengers talking about British Airways, there is no shortage of complaints. Listening to shareholders in BA’s parent company International Consolidated Airlines Group (LSE: IAG) however, I would be surprised to hear many complaints about recent performance. It was the best performer in the FTSE 100 index last year – and the IAG share price has doubled over the past year.

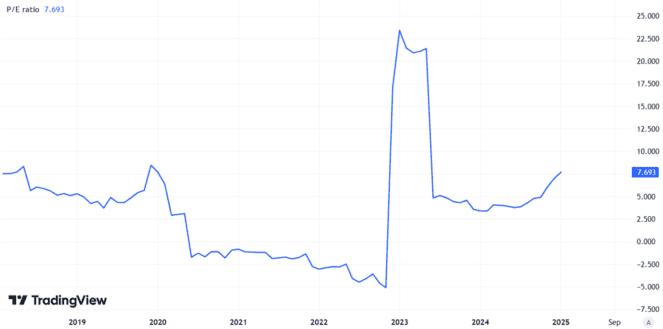

Despite that, the price-to-earnings (P/E) ratio continues to look relatively cheap. At 8, not only does it look pretty modest in absolute terms, it is also well off its highs over the past several years.

Created using TradingView

So, is there room for further share price growth at IAG – and ought I to invest?

Things could get better from here

I reckon there could be space for the stock to move up even more.

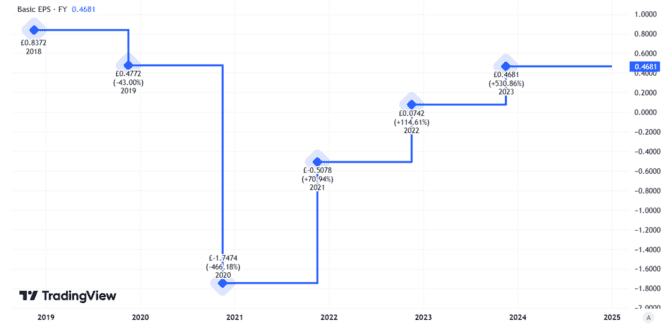

A key reason for the positive mood among investors over the past year is that IAG’s business performance has been improving. A look at the earnings per share demonstrates this.

Created using TradingView

Things are not yet back to where they were in say, 2018, but the direction of travel has been consistent and positive.

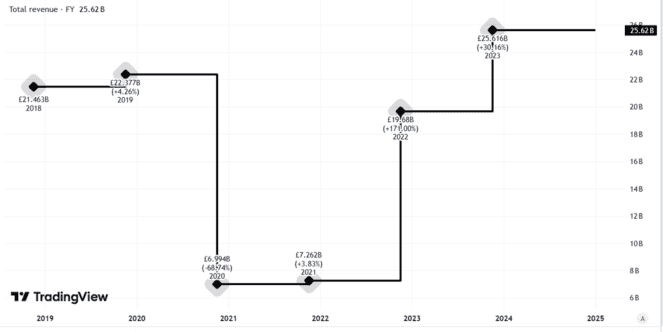

Revenue meanwhile, is ahead of where it stood in 2018. So, if the company keeps a tight rein on costs, that ought to provide an opportunity for profits to move even higher.

Created using TradingView

In the first nine months of last year, net debt fell by around a third. In November the company launched a share buyback, which I take as a sign of financial confidence on the part of the board (though personally I would be more attracted by the money being used to pay down debt or boost the dividend).

Civil aviation demand has been high and the company has struck a positive note about the outlook for this year without yet getting into detailed forecasts.

Am I ready to invest?

However, I have some concerns.

One is what IAG’s years of relentless cost-cutting and testing passengers’ loyalty mean for the business over the long term Yes, lately it has been trying to elevate elements of the passenger experience. But I think that is a reflection of its realisation that it had increasingly lost key competitive advantages as customers questioned why they should shell out big money for airlines with little in the way of service on many routes.

I also see a risk that, when the next big demand shock comes for civil aviation, it could once again hurt revenues, profits – and the share price.

From pandemics to terrorist attacks and recessions, such external shocks tend to pop up from time to time and sit outside IAG’s control to a large extent (or completely).

So while I think the share price could keep moving up, I do not like the risk profile at the current price and so have no plans to invest.