Over the last 12 months, the Shell (LSE:SHEL) share price has fallen around 7%. And the company is about to report its earnings for the third quarter of 2024.

It looks likely that profits are going to come in lower than they did a year ago. But with the stock already down, is the bad news priced in?

A difficult setup

There are two reasons Shell’s earnings are expected to be weaker than they were in 2023. One is that things were exceptionally strong then and the other is that they’re more difficult now.

Earlier this week, BP reported its lowest quarterly profit since 2020. And the company identified weaker refining margins as a key reason for this.

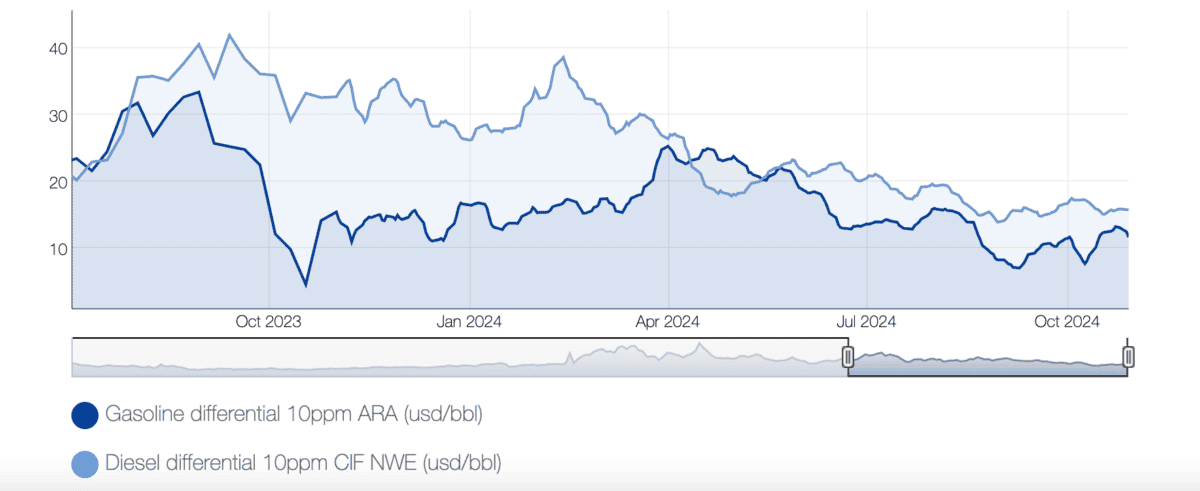

Gasoline & diesel refining margins Q3 2023-present

Source: Neste.com

It’s absolutely true that diesel and gasoline margins are lower than they were a year ago – and this is the same for Shell as it is for BP. But lower refining differentials aren’t the only issue.

BP also stated its trading revenues had normalised after an unusually strong Q3 2023. Shell also reported an impressive performance in its trading a year ago, so that’s also likely to be lower.

Outlook

These factors mean I’m not expecting much in the way of positive surprises from Shell when it reports earnings on Thursday (31 October). But the bigger issue for the investors is the future.

In terms of refining margins, the outlook is somewhat mixed. While the gasoline differential is roughly where it was a year ago, the spread on diesel is still much lower.

As a result, I’m expecting weakness in refining margins to continue into Q4 of this year. And the outlook for oil prices more broadly is also challenging in the near term.

The supply side of the equation looks strong, while the demand side looks weak. Ultimately, that means prices are unlikely to rise until something changes.

A buying opportunity?

All of this means there’s not a lot of cause for optimism around Shell – and oil companies in general. But sometimes, the best time to buy can be when everyone else is looking elsewhere.

With Shell specifically, I’m not quite sure this is the moment, though. A look at where the stock has been trading in terms of its price-to-book (P/B) ratio over the last 10 years is interesting.

Shell P/B ratio 2015-24

Created at TradingView

The current share price implies a P/B multiple of 1.15, which is roughly in the middle of the historical range. To me, that doesn’t say investors are particularly worried right now.

Given this, I’m inclined to think the market might be looking past the company’s short-term issues. And while that’s commendable, it doesn’t really make for a buying opportunity.

Keep watching

I don’t have huge expectations for Shell ahead of the company’s Q3 earnings. The business is facing a much more difficult set of trading conditions than it was last year.

I actually think this is likely to continue, but I’m not convinced the current share price reflects this. So I’m going to keep this one on the watchlist and look elsewhere for opportunities.