I’m searching for the best FTSE 250 growth stocks to purchase today. Games Workshop (LSE:GAW) and Greggs (LSE:GRG) are near the top of my shopping list.

Here’s why I think their share prices may shoot through the roof in 2025.

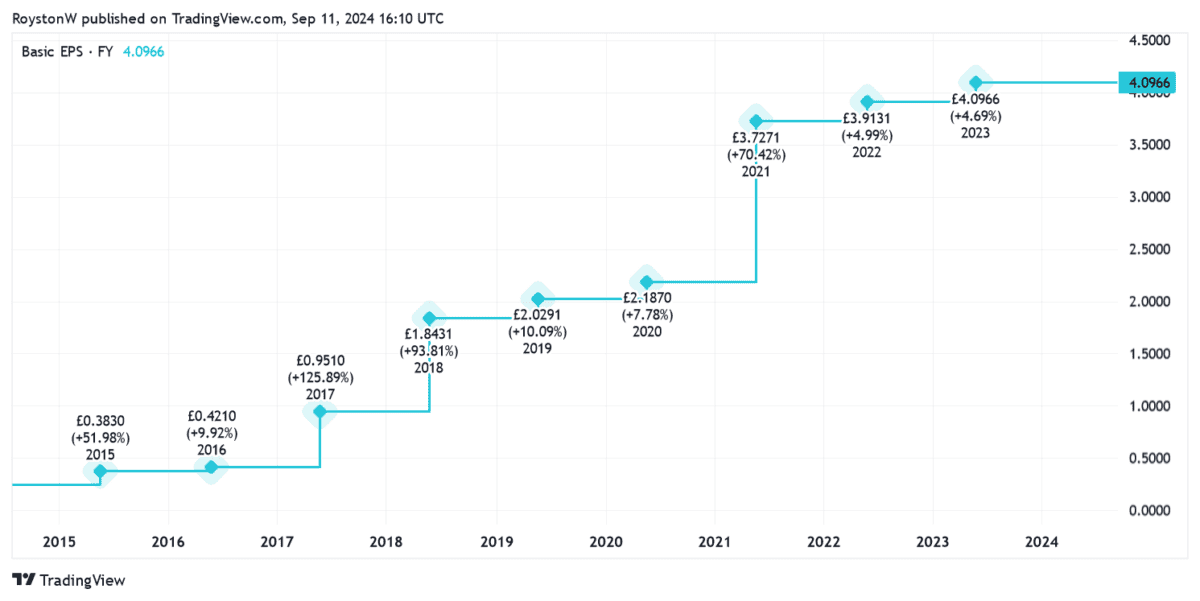

Games Workshop

Games Workshop isn’t tipped to deliver spectacular profits growth in its 2025 financial year. In the 12 months to May, City analysts expect the bottom line to swell just 2% year on year.

But make no mistake, this will still represent an impressive result given last year’s record profit. This remains one of the FTSE 250‘s hottest growth shares, in my opinion, and one I believe could eventually seal a place on the FTSE 100.

Fresh news on Games Workshop’s film and TV content partnership with Amazon could significantly boost its shares next year. Since December, the company’s been collaborating with the streaming giant to adapt its fantasy worlds for the screen. It’s a strategy that could elevate both product sales and royalties to new heights.

As you can see, the company grew annual earnings significantly between fiscal 2014 and 2023. And they rose by an impressive 12% last year, to 458.2p per share, helped by the new blockbuster Warhammer 40,000 product releases.

The business has plans to open even more stores in North America and Europe too, to keep the bottom line growing.

The Games Workshop share price has risen 6% to date in 2024. I’m expecting even bigger gains next year, although a meaty price-to-earnings (P/E) ratio of 22.3 times might be a drag on performance. It might actually cause the price to drop if trading conditions worsen, which they could.

Still, on balance, things are looking good for the hobby giant next year.

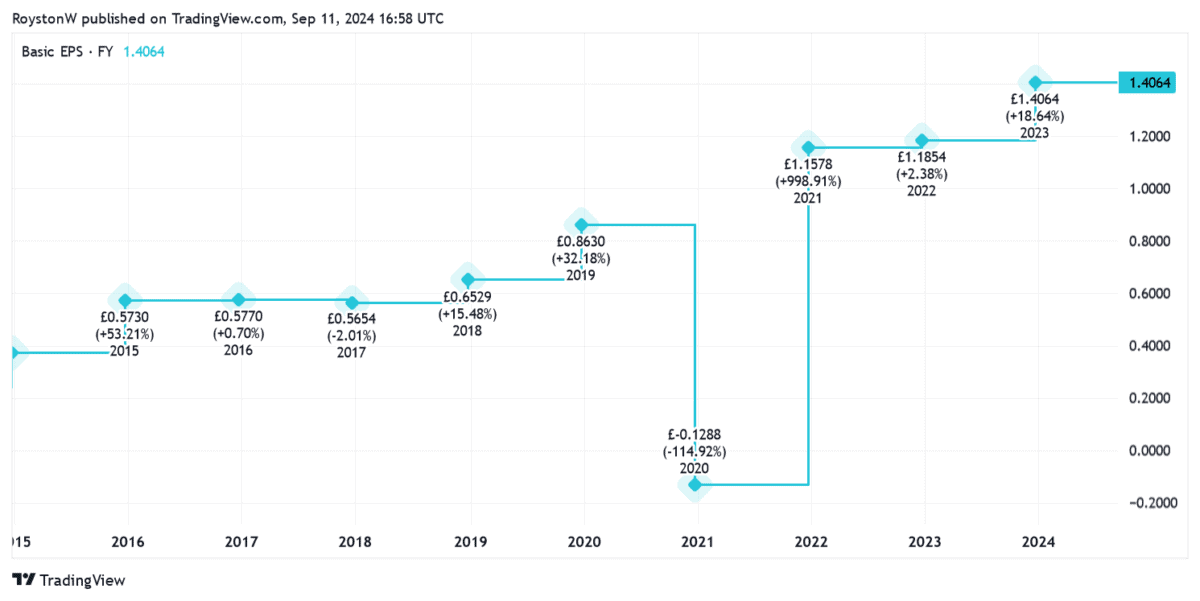

Greggs

Baked goods giant Greggs hasn’t had the same sort of sustained earnings growth as Games Workshop. Indeed, profits were battered during the pandemic as the firm was forced to close shops during lockdowns.

But excluding the Covid-19 crisis, this FTSE 250 stock’s largely delivered solid profits expansion over the period, as the chart below indicates.

Earnings were driven by a significant increase in the number of shops Greggs operates. And with store openings continuing at a healthy clip, City analysts are expecting earnings to rise another 7% this year before accelerating to 10% in 2025.

The baker now sells its tasty treats from just over 2,500 shops. That’s up 52% from the number seen a decade ago, and Greggs isn’t done yet. It hopes to have 3,500 shops up and running eventually.

Encouragingly, the company’s also investing heavily in its online channel to bring further growth. And it’s working to open two new manufacturing sites over the next few years to boost capacity. Of course execution risks exist that could hamper the firm’s ambitious growth strategy however.

Greggs’ share price has soared an impressive 19.6% since the beginning of 2024. I’m expecting another strong performance in 2025.