I’ve been building up a position in an exciting growth stock for some months now. Thankfully, the investment platform holding my ISA offers free trading, so I’ve been nibbling away at the shares every time they have dipped. They’re now just $1.68 (about £1.39) apiece.

The stock I’m talking about is Ginkgo Bioworks (NYSE: DNA). Here’s why I’m bullish.

A cell-programmer

Ginkgo Bioworks is a synthetic biology company that aims to program cells as easily as we can program computers. Its bio-engineering foundry helps its customers make everything from fragrances and biodegradable plastics to plant-based foods and cannabis products.

The thing I like here is that Ginkgo doesn’t create its own products, meaning its platform is agnostic.

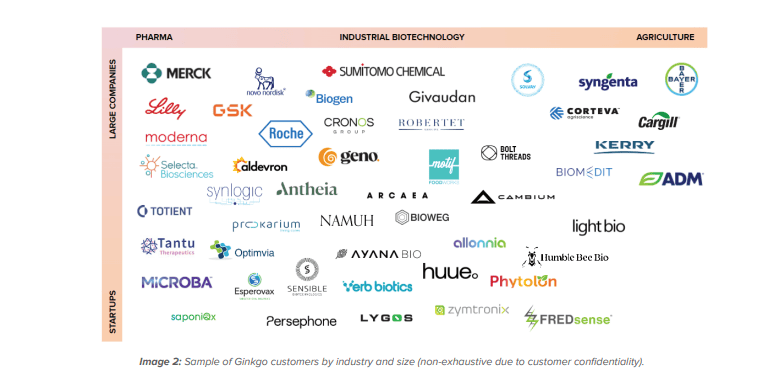

That’s why it currently has program partnerships with the likes of Moderna and Pfizer (rivals to each other). And it just signed a drug-discovery collaboration with the latter worth up to $331m in fees and milestone payments, with further potential for royalties.

Potentially powerful business model

The company’s cell-engineering foundry is a highly automated laboratory powered by robotics and software. So that means there aren’t many scientists holding pipettes at workbenches.

Indeed, the firm claims its automation produces 10 times the output of scientists working by hand. This means there is significant potential cost and efficiency gains for companies outsourcing research and development (R&D) to Ginkgo. And this should attract more customers and R&D spending to its platform.

Additional programmes will also increase Ginkgo’s vast ‘Codebase’ of biological data used to program cells. It added 21 new programmes to its platform in Q2, with companies including Sumitomo, Novo Nordisk, and Merck. It intends to add 100 new ones in total throughout 2023.

As well as charging customers upfront, the firm is entitled to potential further downstream value in the form of royalties on sales.

Of course, in the case of the dozens of start-ups that also use its platform (in which it takes equity stakes), there’s a risk those products never materialise.

Big risks

Now, the company remains deeply unprofitable, meaning its business model is still unproven.

It expects total revenue of between $245m and $260m this year, down from $477m last year as various Covid-testing revenue disappears. But it has burned through $297m of cash over the last 12 months. The risk here is that the firm never scales up fast enough to make a profit.

Plus, trading on a price-to-sales (P/S) ratio of 10, the shares are far from cheap, even at the equivalent of £1. So this is a highly speculative stock that isn’t suited to risk-averse investors. And I’m aware this one could flop badly (even more than it has already).

Nevertheless, I see a lot of long-term potential here. And I’m intrigued by a recent deal Ginkgo announced with Google Cloud to develop large language models for bio-engineering purposes.

The aim is for this artificial intelligence system to learn to speak DNA just like ChatGPT learned English. The eventual applications here could be far-reaching.

Finally, I note that the stock is currently worth nearly 2.5% of ARK Invest’s various portfolios. And it has been held by Scottish Mortgage Investment Trust for a number of years.

So the firm has smart backing, as well as a remaining cash runway of $1bn.