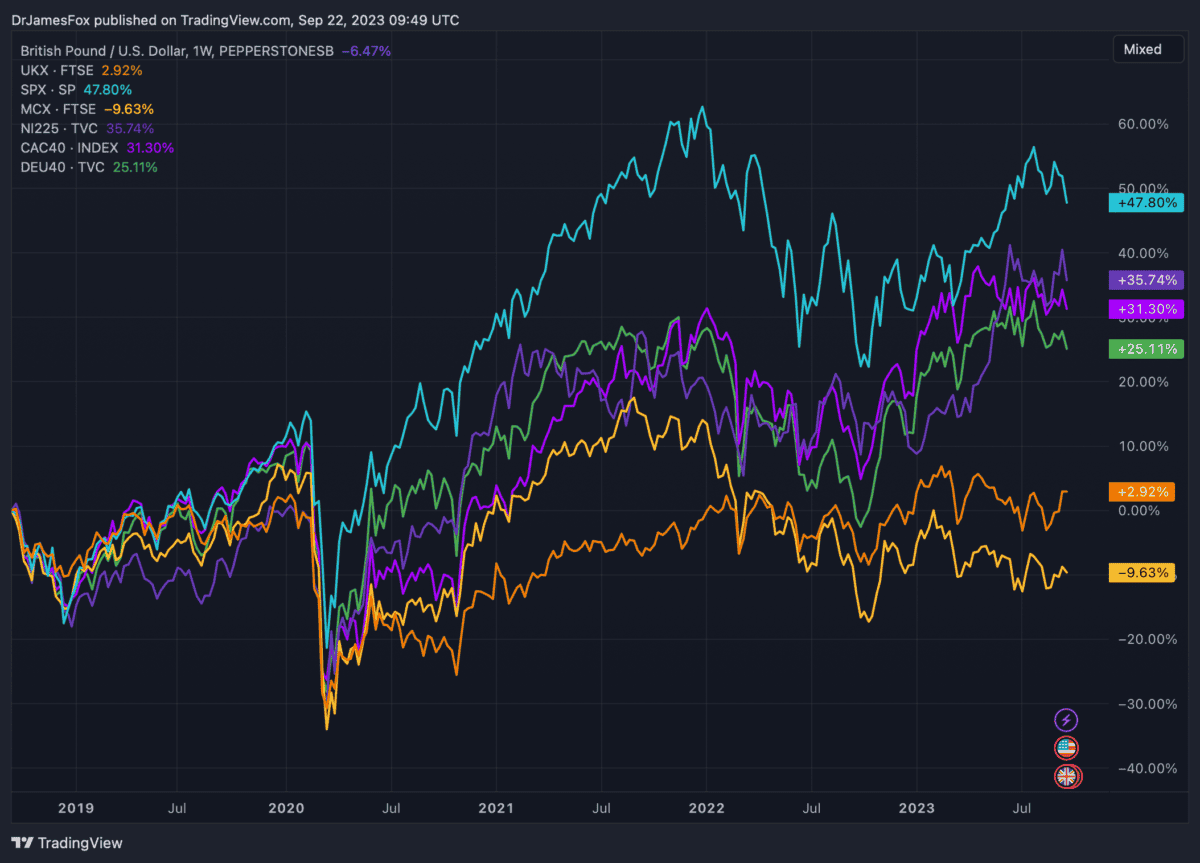

UK stocks are well represented in my portfolio. That’s created some challenges in recent years as UK equities have experienced a slower pace of growth than their international counterparts.

While the recent performance has been poor, this doesn’t reflect a downturn in earnings. As such, we can see that valuations among UK stocks are considerably below their US peers — where the stock market has surged 47.8% over five years.

So my two largest holdings are both UK stocks, and they’re both, in my view, substantially undervalued. Here they are…

Barclays

Barclays (LSE:BARC) represents around 10% of my stocks and shares portfolio. The banking giant certainly isn’t an investor favourite, with sentiment possibly still damaged from the 2008 banking crisis.

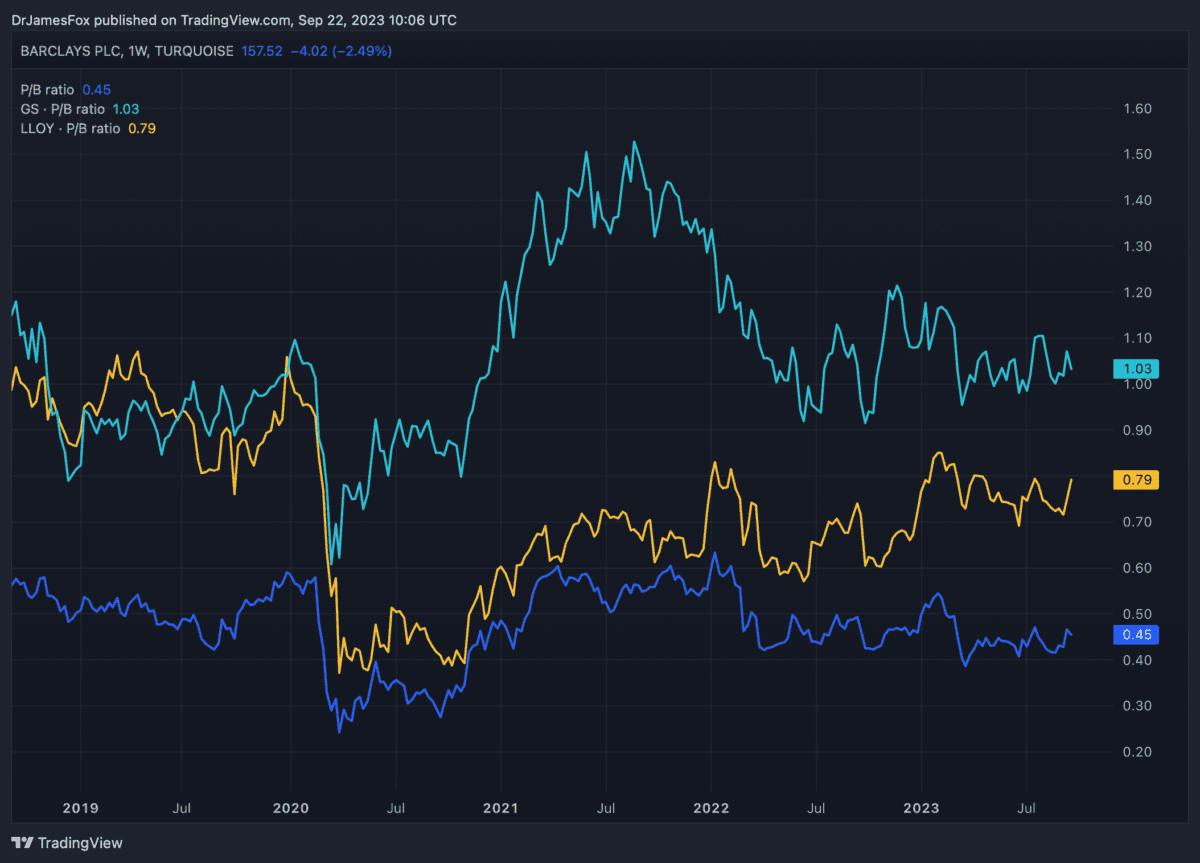

The stock currently trades at just 5.2 times earnings and has a price-to-book ratio of just 0.45 times. In turn, this infers a huge 55% discount versus the bank’s tangible net asset value.

On a P/E basis, it trades at a fraction of the index average, which is around 12 times, and substantially below the financial sector average, around 10.8 times.

The chart below shows how pronounced the discount is versus two of its peers. US-listed banks tend to trade near or above their book value. Interestingly, in 2022, Barclays’s revenue generated in the US was substantial — around a third of UK revenue.

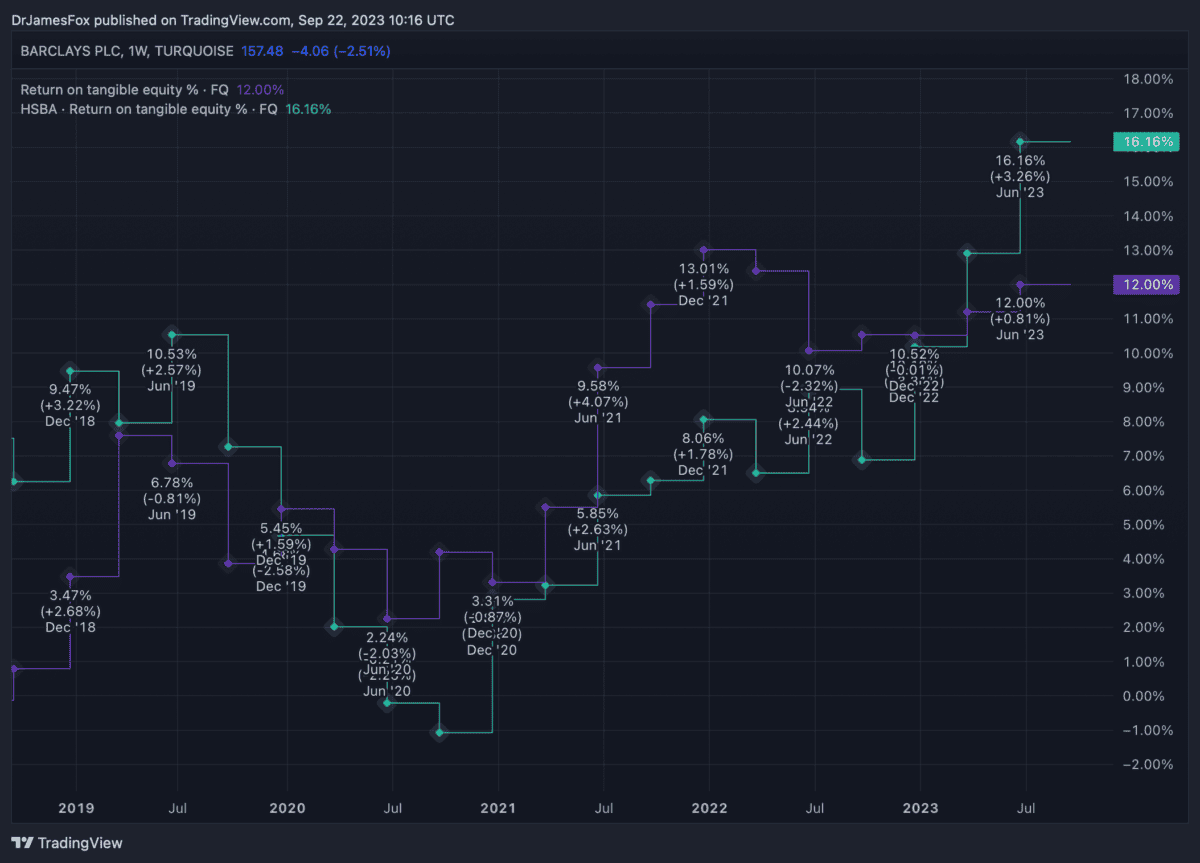

However, Barclays is traditionally less efficient at generating returns than some of its peers. This is demonstrated by the company’s lower-than-average return on tangible equity (RoTE). The chart here compares Barclays’s RoTE with HSBC’s.

This is clearly a disadvantage, but in an improving environment, whereby interest rates in the UK moderate towards the ‘Goldilocks zone’, I’m more than confident this will improve.

Hargreaves Lansdown

Hagreaves Lansdown (LSE:HL) is my second-largest holding, also representing around 10% of my holdings.

Recent results highlighted the robust nature of the business, with net interest income soaring as interest rates reach levels unseen for decades.

Combined with the falling share price — the stock is down 56% since its Covid era peak — Hargreaves looks cheaper than ever. We can see this in this following chart.

Personally, I see this as a great opportunity to pick up more shares. Despite increased competition, market share has remained steady.

However, I’m partly of the opinion that Hargreaves may need to offer some price incentives to continue growing its market share. It’s service, data, and platform are second-to-none, but as Britons return to investing after the cost-of-living crisis, Hargreaves needs to be in pole position.

Moreover, in addition to considerable upside as highlighted by the valuation and sector growth potential, the stock offers a 5% dividend yield. I believe Hargreaves can power my way to double-digit returns over the medium term.